Are You Managing a Supplier or Competing for Supply?

How Feedstock, Capacity, and Compliance Are Reshaping the High-Performance Magnet Market

For decades, sourcing high-performance permanent magnets was largely a procurement exercise.

Engineering released a design.

Purchasing issued an RFQ.

Suppliers competed.

A purchase order was awarded.

The process was not perfect.

But it generally worked because supply existed.

Today, that assumption deserves a second look.

Across portions of the aerospace and defense market, the question is no longer simply:

“Who can make the part?”

Increasingly, the question is becoming:

“Who has access to the material, capacity, and supply chain required to make the part?”

The distinction may seem subtle.

It is not.

Organizations that understand the difference may find themselves with more options available than those who continue managing only one layer of the supply chain.

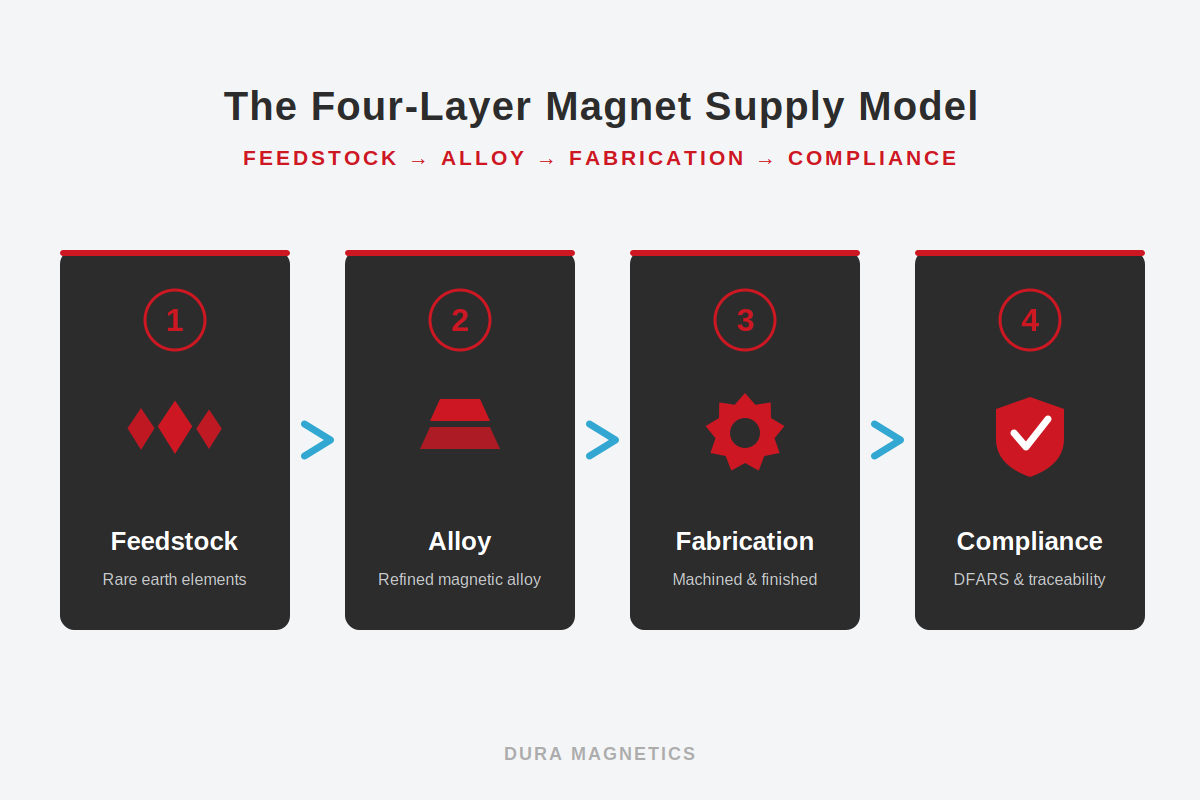

The Four-Layer Magnet Supply Model

Many sourcing discussions focus exclusively on the finished magnet.

In reality, the supply of high-performance permanent magnets used in aerospace, defense, medical, and other demanding applications depends upon four interconnected layers:

Feedstock → Alloy → Fabrication → Compliance

A disruption at any layer affects every layer above it.

Organizations that understand only one layer often find themselves reacting to supply-chain changes.

Organizations that understand how the layers interact typically have more options available when conditions change.

Layer 1: Feedstock

Rare earth materials such as samarium, dysprosium, and terbium form the foundation of many high-performance permanent magnets.

These elements are often used because they enable magnetic properties required for demanding applications, including elevated operating temperatures, resistance to external demagnetizing fields, or both.

Without feedstock, there is no alloy.

Without alloy, there are no magnets.

Historically, many organizations focused primarily on the availability of finished magnets.

Increasingly, attention is shifting upstream.

The reason is straightforward.

The availability of high-performance magnetic materials ultimately depends upon access to the rare earth elements required to produce them.

Recent export controls and evolving sourcing requirements have drawn additional attention to these feedstocks because many existing supply chains remain dependent upon them.

Layer 2: Alloy

Feedstocks must be converted into usable magnetic alloys.

This is where many organizations assume the supply chain challenge begins.

In reality, alloy production is increasingly influenced by feedstock availability, material traceability, export controls, and future sourcing requirements.

As a result, alloy availability is no longer determined solely by manufacturing capability.

It is increasingly influenced by access to qualified feedstocks.

Layer 3: Fabrication

Once alloy is available, it must be transformed into finished magnets.

Slicing.

Grinding.

EDM processing.

Coating.

Magnetizing.

Inspection.

Assembly.

Fabrication capacity is often overlooked because it is less visible than feedstock or alloy sourcing.

However, fabrication resources remain finite.

Several manufacturers have continued investing in additional processing capacity over the past several years.

Yet lead times remain elevated because demand absorbs newly available capacity almost as quickly as it is added.

Capacity expansion alone does not necessarily eliminate supply constraints.

Layer 4: Compliance

Historically, compliance was often viewed as a downstream activity.

Today, compliance considerations increasingly influence sourcing decisions throughout the supply chain.

DFARS requirements.

Export controls.

Country-of-origin considerations.

Customer flow-down requirements.

Qualification obligations.

Compliance is no longer a standalone function.

It has become a factor influencing sourcing strategy, inventory planning, supplier selection, and long-term capacity decisions.

Why Aerospace Companies May Be More Exposed Than They Realize

Many defense programs have operated within constrained sourcing environments for years.

Commercial aerospace programs often have not.

Historically, commercial programs could source magnets through global supply chains optimized for cost, performance, and availability.

Defense programs operated under a different set of requirements.

For years, those ecosystems largely coexisted.

That separation is becoming less clear.

As export controls introduce additional friction into portions of the commercial magnet market, organizations that previously relied upon established sourcing pathways are increasingly evaluating alternatives.

One aerospace manufacturer recently spent months pursuing a traditional supply path only to ultimately pivot toward Western sources, where it then encountered a different constraint: material availability.

The result is an emerging convergence of demand.

Commercial aerospace.

Defense.

Industrial.

All seeking access to a smaller pool of qualified feedstocks, alloy production capacity, fabrication resources, and technical expertise.

The challenge is no longer isolated to defense programs.

The 2027 DFARS Discussion May Be Missing the Real Issue

Much of the attention across aerospace and defense organizations that depend upon high-performance permanent magnets is understandably focused on future compliance requirements.

However, supply chains rarely wait for regulations to become effective before responding.Dura Magnetics works with engineering and sourcing teams to map exposure across all four layers (feedstock, alloy, fabrication, and compliance) and build sourcing strategies that hold up when conditions change.

Material suppliers secure feedstocks.

Manufacturers allocate production capacity.

Customers pursue alternate sourcing paths.

Inventory is reserved.

Qualification efforts begin.

Markets adapt.

In practice, many of the conditions that will influence future compliance are already influencing supply-chain behavior today.

The challenge is not simply achieving compliance in 2027.

The challenge is understanding whether the feedstocks, alloy production, fabrication capacity, and qualification pathways required to achieve compliance will remain available when they are needed.

Symptoms of an Allocation Market

Most organizations are familiar with procurement-driven markets.

Allocation-driven markets behave differently.

You may already be operating in an allocation-driven environment if you observe:

Increasing material prices despite long-standing supplier relationships.

Suppliers discussing feedstock availability rather than manufacturing capability.

Customers seeking raw material availability before discussing part fabrication.

Qualification activity increasing as organizations pursue alternate sourcing strategies.

Engineering teams evaluating material substitutions that would not have been considered several years ago.

Purchasing teams spending more time securing supply than negotiating price.

Program schedules becoming dependent upon material availability rather than manufacturing cycle time.

Suppliers reserving inventory for strategic, long-term, or higher-priority programs.

None of these symptoms independently prove a supply-chain crisis.

Collectively, however, they may indicate that market participants are beginning to allocate feedstocks, alloy production, fabrication capacity, and inventory rather than treating them as readily available commodities.

When allocation begins influencing sourcing decisions, traditional procurement strategies often become less effective than supply-chain visibility, qualification planning, and long-term supplier relationships.

What This Looks Like in Practice

The shift toward allocation is not merely theoretical.

Across the industry, organizations are increasingly encountering situations where material availability drives decisions that historically would have been based primarily on price, quality, or delivery.

Several large aerospace and defense organizations have shifted from asking whether a supplier can manufacture a part to asking whether alloy exists at all.

Manufacturers continue investing in additional processing capacity, yet lead times remain elevated because demand quickly absorbs newly available resources.

Material costs have increased significantly in certain product categories while delivery timelines have expanded well beyond historical norms.

The market may still appear functional.

Parts continue to ship.

Programs continue to move forward.

Capacity continues to be added.

Yet many of the behaviors historically associated with abundant supply, stable lead times, predictable pricing, broad supplier availability, and transaction-based procurement, are increasingly being replaced by behaviors associated with allocation-driven markets.

Four Questions Worth Asking Today

Organizations supporting aerospace and defense programs may benefit from asking:

1. Do we know where the critical materials supporting our products originate?

Many organizations know their direct supplier but have limited visibility into upstream supply chains.

2. What is the actual bottleneck in our supply chain?

Feedstock?

Alloy?

Fabrication capacity?

Qualification timelines?

The answer may not be where you expect.

3. How dependent are we upon a single supply pathway?

If a material source, alloy producer, or fabrication provider becomes constrained, what alternatives exist?

4. Are we managing suppliers or competing for supply?

The distinction may become increasingly important as demand concentrates within a smaller number of qualified supply chains.

Looking Forward

For many organizations, the frustration may not stem from poor execution.

It may stem from a misunderstanding of the problem itself.

We thought we were managing suppliers.

We didn’t realize our success depended upon supply chains we neither owned nor controlled.

When supply is abundant, procurement tools are often sufficient.

Organizations issue RFQs.

Suppliers compete.

Purchase orders are placed.

The market functions efficiently.

However, as feedstock availability, alloy production, fabrication capacity, and compliance requirements become increasingly interconnected within an allocation-driven environment, supplier management alone may no longer provide adequate visibility into risk.

A supplier may perform exactly as expected.

An alloy producer may perform exactly as expected.

A manufacturer may perform exactly as expected.

Yet a program can still experience disruption because the constraint exists elsewhere within the supply chain.

The organizations best positioned for the future may not be those with the largest supplier base.

They may be the organizations that best understand the systems upon which their suppliers depend.

The future of the high-performance magnet market will not be determined by a single regulation, supplier, or technology.

It will be shaped by the interaction of feedstock availability, alloy production, fabrication capacity, and compliance requirements.

Organizations that understand only one layer of the system may find themselves reacting to events.

Organizations that understand how the layers interact will likely have more options available when change occurs.

The question may no longer be whether a supplier can manufacture a magnet.

Increasingly, the more important question may be whether the entire supply chain supporting that magnet remains available when it is needed.

Understanding your supply chain is the first step to protecting it.

Dura Magnetics helps engineering and sourcing teams map their exposure across all four layers (feedstock, alloy, fabrication, and compliance) and build sourcing strategies that hold up when conditions change.

The permanent magnet industry is approaching a major regulatory shift, one that has been quietly building for years but may still be flying under the radar for many OEMs, engineers, and supply-chain teams. While the headlines have focused on the Trump Administration’s 2025 “Executive Tariffs,” another set of tariffs, the long-planned Section 301 increases, will...

Recent reports that China has begun issuing “general” export licenses for heavy rare earth (HREE) materials have been widely interpreted as a sign that the rare earth magnet market may soon normalize. While these developments are directionally positive, they should not be mistaken for a near-term solution to the backlog of blocked shipments, delayed orders,...

The global market for samarium cobalt (SmCo) magnets is under exceptional pressure. A convergence of export controls, raw material restrictions, and cost volatility is reshaping how these high-performance magnets are sourced and priced. This update summarizes the current conditions influencing availability, outlines the outlook for the next year, and explains how Dura Magnetics is managing...